There are already many signs that the economy has hit bottom. It is doing so barely above the level we had in 2018. Over seven years, cumulative growth amounts to 5.5%, or 0.75% per year. That is far from the 2.3% average of the previous forty years. Expectations for this year and the next do not return to that average, but they do exceed what we have seen over the past seven years. It is not clear to me why we would obtain a different result if economic policy is essentially the same. On the contrary, it is possible that some of the damage is already structural.

In essence, the economic “strategy” seems centered on two elements. One is the rapid increase of the minimum wage; the other is the displacement of the private sector, especially in energy. These two elements have been in place since the beginning of López Obrador’s administration. After the 2021 election, an irresponsible fiscal policy was added—one we have described several times—but the first two are characteristic of these administrations.

As is well known, the minimum wage ceased to be relevant after the 1982 crisis. Before that, many people earned less than that benchmark, but by the end of that decade the opposite was true. The issue became a mantra of the left (that is, those displaced from power after 1982), and during Peña Nieto’s term they managed to place it on the public agenda. The links between the minimum wage and all kinds of contracts were eliminated—these had been the mechanism for controlling inflation in the 1980s and 1990s—and thanks to that, it became possible to begin a process that would finally turn the minimum wage into a serious benchmark.

This occurred in 2016, and by 2017 the first significant increase could be implemented. At the time, my opinion was that the minimum wage could be doubled without problems, because practically no one earned less than two minimum wages, either in the formal or informal sector. They chose to do it gradually, and by 2022 it had increased, in real terms, by almost 75%. But by then, López Obrador was already organizing the 2024 election and needed to create the perception of a successful economy. At that point, any illusion of “fiscal responsibility” ended.

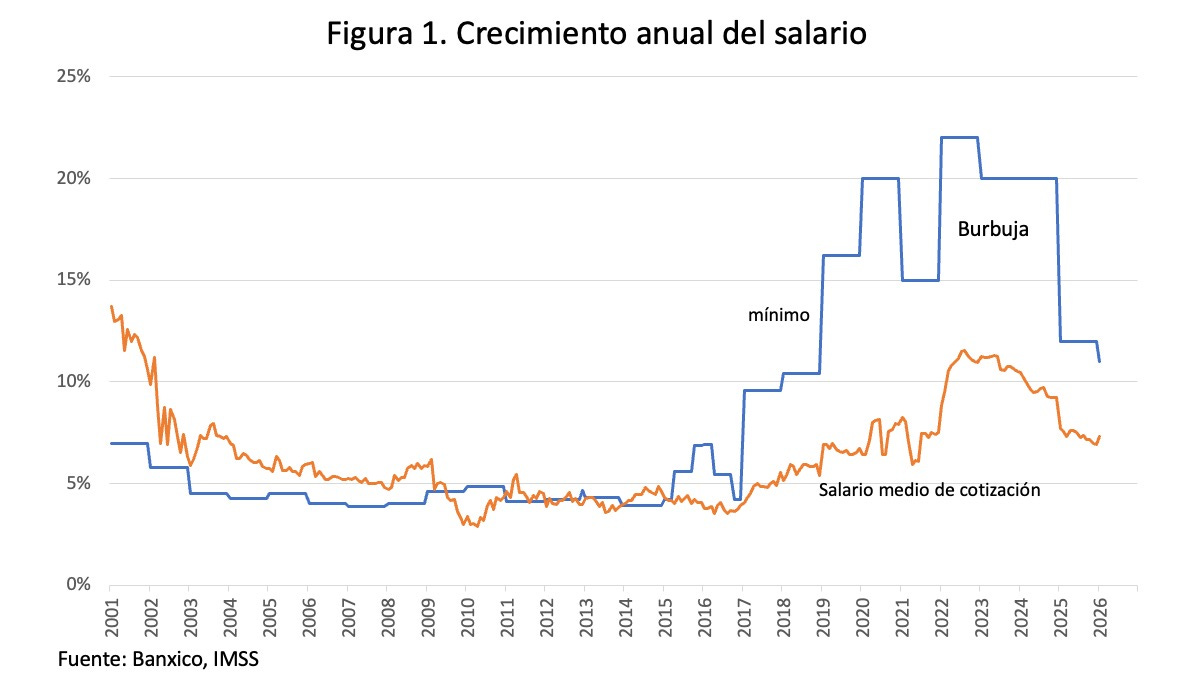

Figure 1 shows the annual increase in the minimum wage and the IMSS average contribution wage since 2001. Clearly, in the first decade of this century the minimum wage had no importance, and the average wage always grew faster. After the Great Recession, both indicators moved together, until the change we have already described occurred.

Note the growth of the minimum wage toward its doubling, which by 2022 had begun to stabilize, followed by the leap in 2023 and 2024 that has no justification other than López’s urgency to win the election. Although increases in 2025 and 2026 are smaller, they still exceed inflation and accumulate on top of the previous bubble, so that by early 2026 the minimum wage is 166% higher in real terms than it was in 2016. In that same period, the average contribution wage grew only 33% in real terms. It is important to consider that part of this latter increase is the pressure generated by the minimum wage: it is illegal to pay less than one minimum wage.

With these increases, the minimum wage has gone from representing between 20 and 25% of the average wage to now exceeding 45%. On a previous occasion I showed you the comparison with the median wage—the wage earned by the person exactly in the middle of the distribution—and it had already surpassed 60%. I mentioned then that this level is considered very risky internationally. Now I will simply show the comparison with the average wage, in Figure 2.

I added a red line indicating how the minimum wage could have been doubled by this year, so that you can see the difference with what was actually done. The minimum wage this year should be 240 pesos per day, instead of the 309.50 pesos that must be paid.

As always, some will argue that 240 pesos is too little. But that is not the issue; the issue is whether a day of work produces enough to be able to pay that amount. One must not forget that legal benefits add roughly 60% to that cost. According to the evidence, that is not the case, and we have therefore seen a continuous reduction in the number of registered employers over the past two years: the increase in the minimum wage has already become a problem.

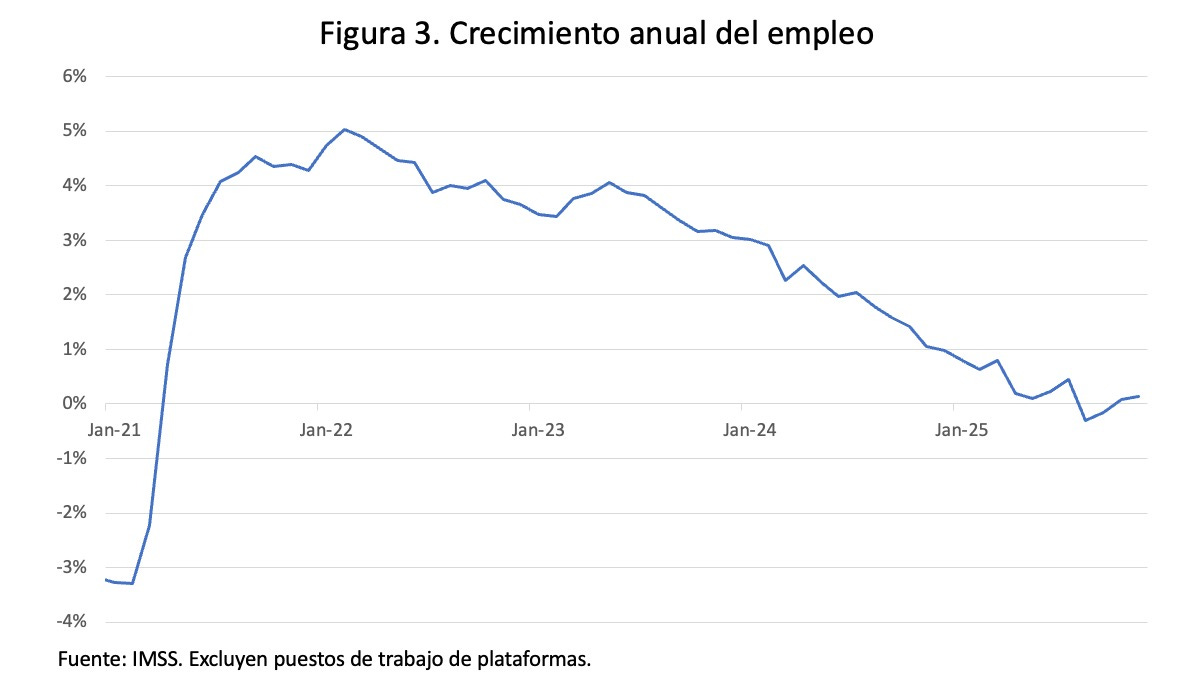

This can be seen in job creation, shown in Figure 3. Rates reached as high as 5% during the post-pandemic recovery, fell to 4% at the beginning of 2023, and since then have dropped to practically zero.

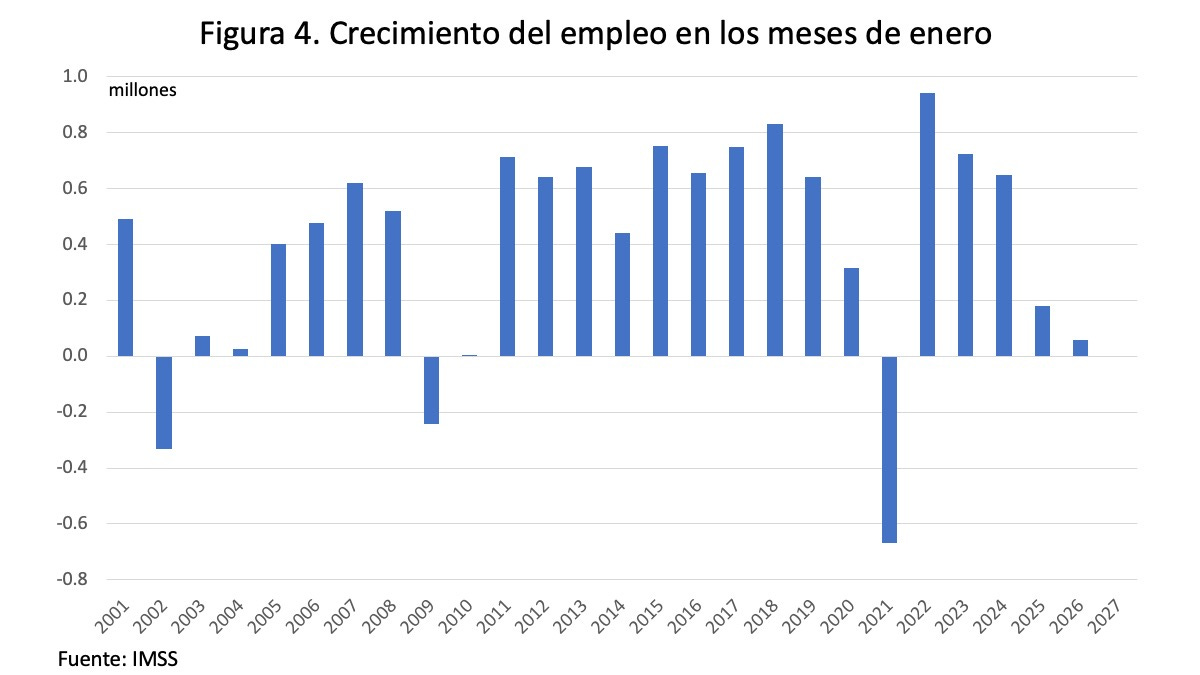

In January we had the lowest job creation of any year, with the exception of the recessions you already know—2001–2003, 2009, and 2020—which are reflected even in an additional year.

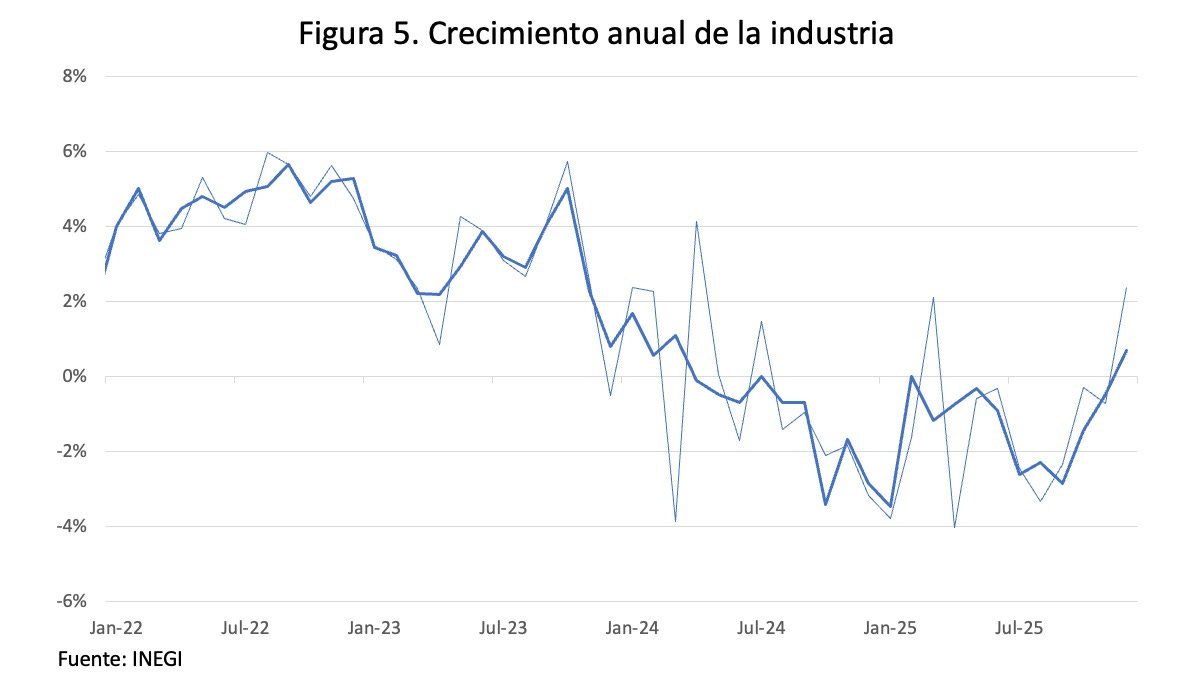

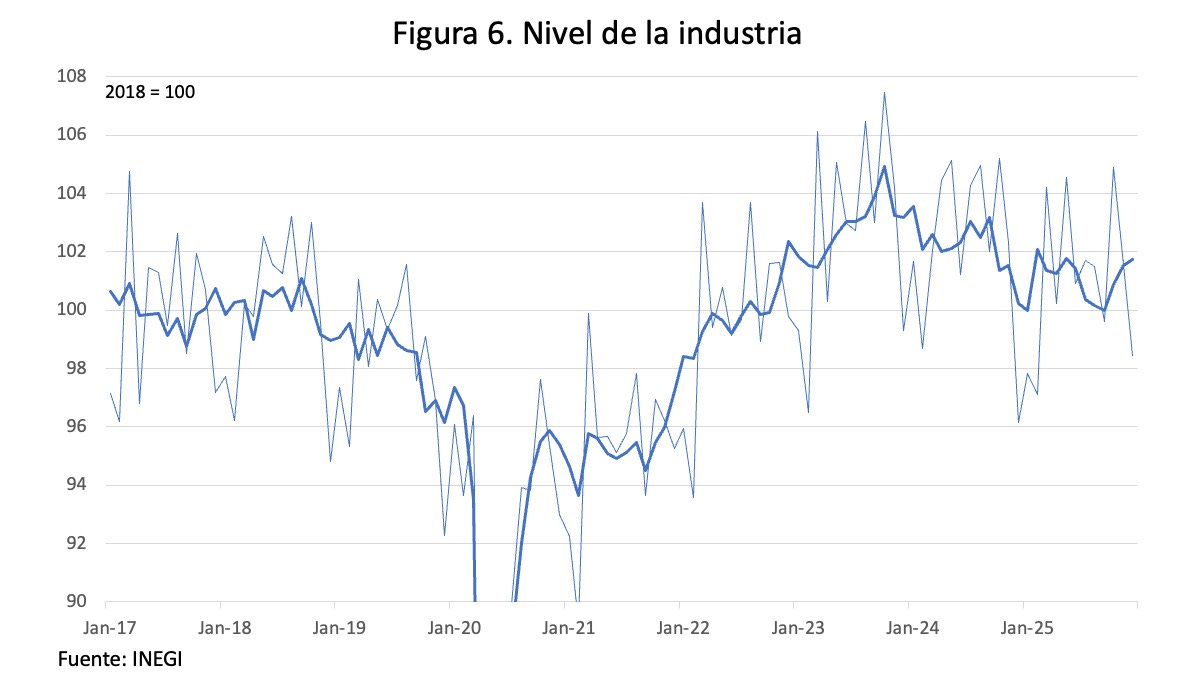

But I was saying that it seems we are at a floor, and Figure 5 shows this phenomenon for industry. After many months in negative territory, December posted a positive figure—the first in nearly two years.

However, when one looks at the level rather than the growth rate, it becomes clear that what we have is not growth but rather a decline that appears somewhat less severe than before, nothing more. From the peak reached in September 2023 we have already lost two full points.

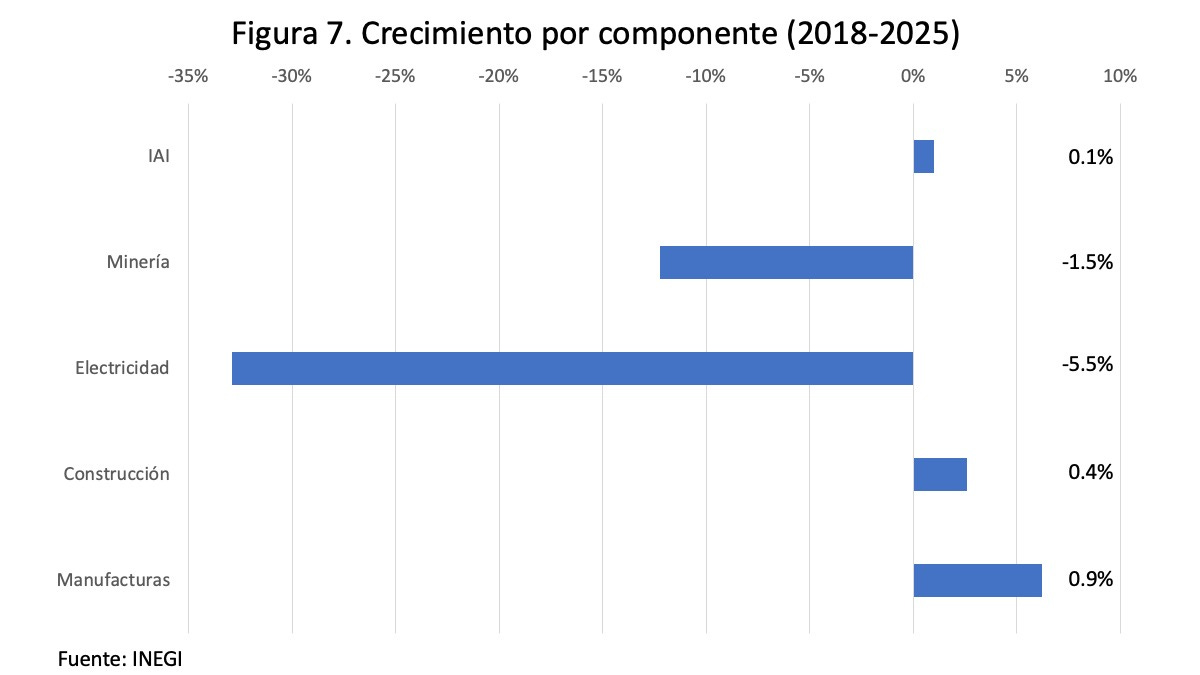

For that reason, cumulative growth since 2018 is almost nil in industry. Figure 7 shows the accumulated performance over these seven years, and I included the average annual growth rate alongside it.

For industry as a whole there is slight annual growth, but in the energy sector the collapse is considerable. Mining (oil) has fallen by -1.5% per year, and electricity by nearly -6%. This drag will be decisive in the coming years, because there is no way to grow without electricity—and they refuse to liberalize the market. Construction has grown at 0.4%, and manufacturing at almost 1% annually, but there is a measurement problem that I will comment on shortly.

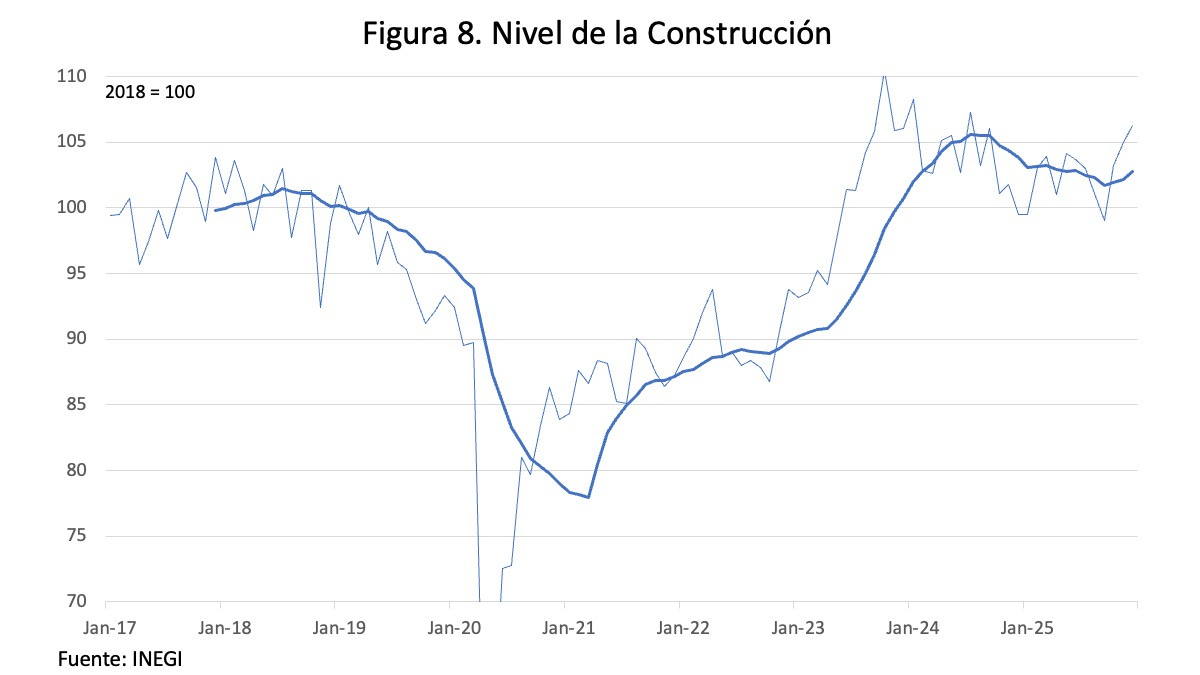

In the case of construction—which had a spectacular close in 2025—the trajectory has been very erratic: it begins to fall with the cancellation of the airport, accelerates with the pandemic, experiences a very slow recovery, accelerates with López’s bubble, and then falls again.

If not for the push in the last quarter, we would be almost at 2018 levels.

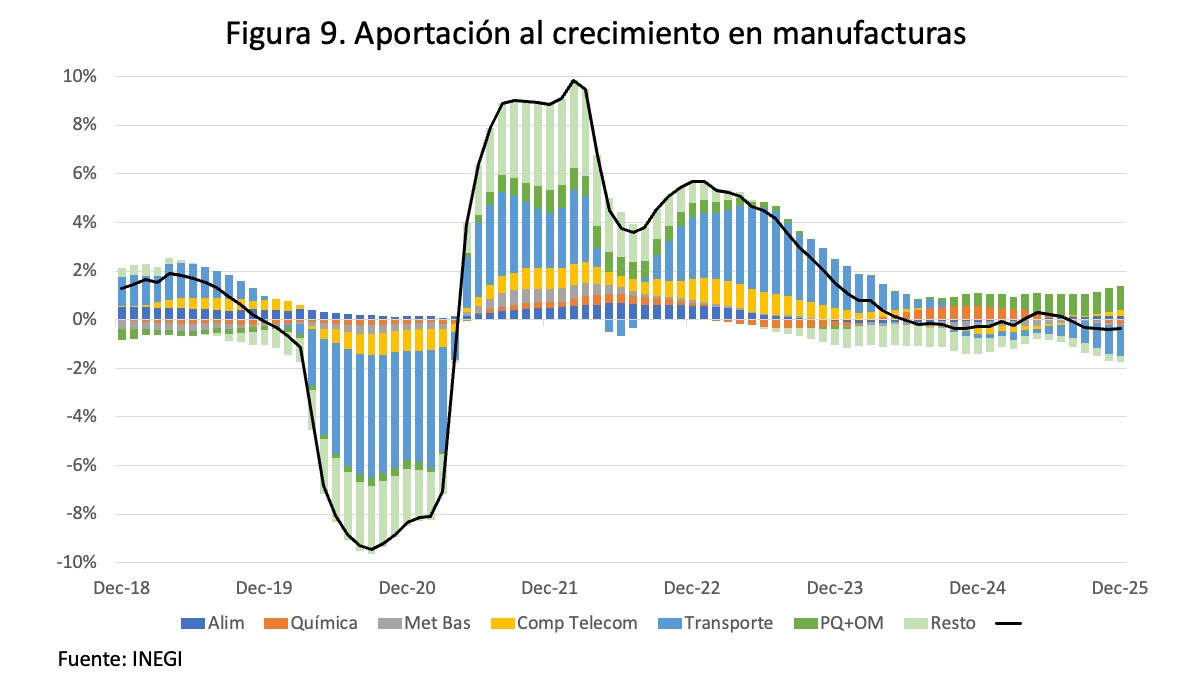

As for manufacturing, as I mentioned, there is a “hidden hand.” It turns out that all of the growth in 2025 occurs in two activities: refining and “other manufacturing.” Figure 9, which we have seen before, shows contributions to growth by activity. The light blue bar is the automotive industry, which is collapsing. The light green bar is the sum of all activities not shown in the figure. The food, chemical, and basic metals industries do appear but are small. The yellow bar, electronic equipment, has performed well, but it is clearly not decisive in 2025.

The only thing growing, as I said, is the dark green bar: refining plus “other manufacturing,” which in fact corresponds to “Manufacture of non-electronic equipment and disposable medical, dental, and laboratory supplies, and ophthalmic articles.” All the growth in “other manufacturing” occurred there.

The refining increase does correspond to a greater volume of crude oil refined. What does not seem appropriate to me is counting it as value added when we lose money on every liter refined. I also have doubts about Pemex’s reports regarding fuel oil and asphalt generated in refining—products of very low (or negative) value. I do not know whether INEGI will later clean up this information and revise it, as happened with construction. For now, I think manufacturing growth—and thus industrial growth as a whole—should be taken with a grain of salt.

In short, it seems we are hitting bottom—but it does not look as though we will rise very far from here.